| Instrument | Dez/25 | Jan/26 | Fev/26 | Share | MoM Δ |

|---|---|---|---|---|---|

| DPF (Total) | 8,635.1 | 8,641.1 | 8,840.7 | 100% | +199.6 |

| Taxa Flutuante (LFT) | 4,166.7 | 4,270.4 | 4,340.9 | 49% | +70.5 |

| Índice de Preços (NTN-B) | 2,239.5 | 2,277.0 | 2,285.5 | 26% | +8.6 |

| Prefixados (LTN / NTN-F) | 1,904.0 | 1,784.3 | 1,885.9 | 21% | +101.6 |

| Câmbio (DPFe) | 324.9 | 309.5 | 328.4 | 4% | +18.9 |

| DPMFi (Local) | 8,309.0 | 8,330.5 | 8,511.3 | 96% | +180.8 |

The primary balance (revenues minus non-interest spending) has been negative for most of the past decade. Forecasting the deficit was perenially hard (see FOCUS consensus) due to macro volatility, mid-year politically driven spending announcements, and other factors, but despite its flaws the 2023 fiscal framework has reduced forecast error.

With Selic at ~14.75% and total DPF near R$8.8 trillion, monthly interest accrual runs ~R$108bn. Because 49% of the stock is LFT (Selic-linked), rate cuts directly reduce this snowball effect, while rate hikes accelerate it. The Feb/26 MoM debt increase of R$199.6bn splits roughly 50/50 between accrued interest and net new issuance.

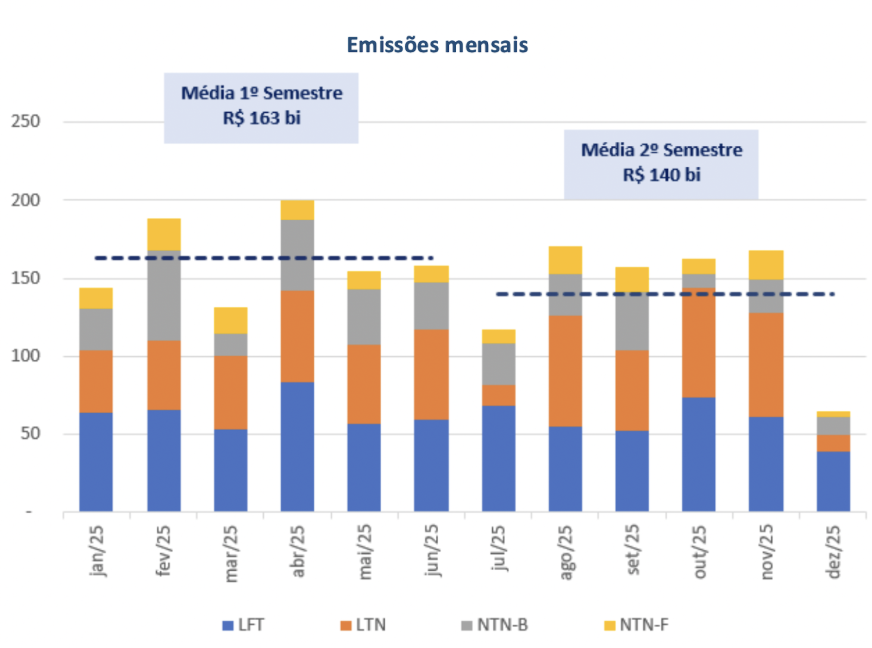

The redemption calendar concentrates around specific instrument maturities. Despite these lumpy maturities, 2025 gross issuance was remarkably stable: H1 averaged R$163bn/month versus R$140bn in H2 — only a ~16% gap. The Treasury smooths issuance through pre-financing and its cash reserve buffer, absorbing maturity spikes without forcing large auction concessions.

Each line shows how market consensus for a given calendar year's primary balance (% GDP) evolved over time. Negative = deficit. Source: BCB FOCUS survey, weekly median.

The Plano Anual de Financiamento (PAF) is published by the Treasury each January, setting indicative composition and maturity targets for the year. Targets are not legally binding — they are guides for issuance strategy, with stated intentions to:

- Increase fixed-rate share (Prefixados) at the margin, reducing Selic sensitivity

- Maintain stable inflation-linked exposure to satisfy pension fund demand

- Gradually extend weighted average maturity (WAM) beyond 3.8 years

- Keep floating share elevated near-term due to investor demand for LFT at current yield levels

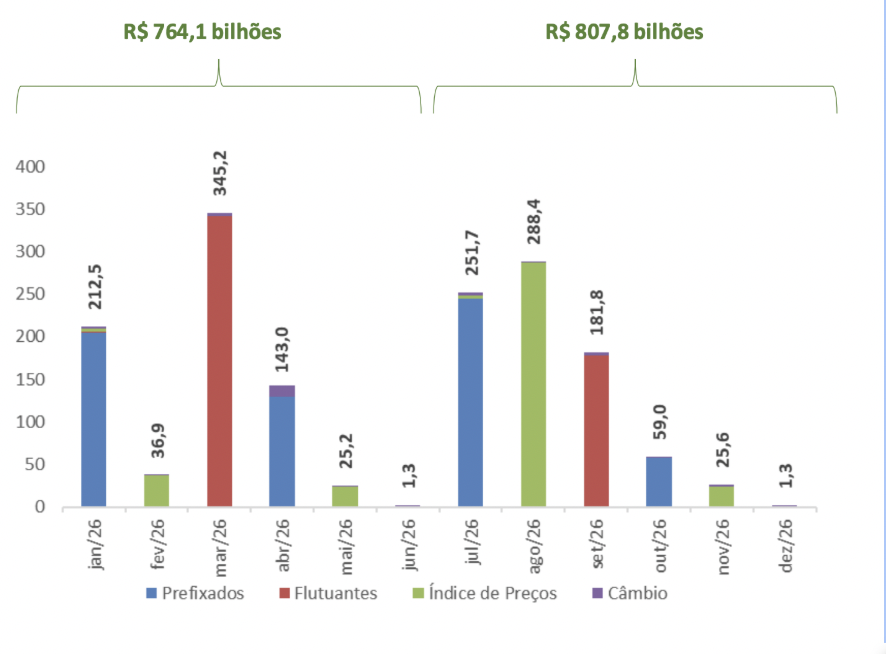

H1/26 = R$764.1bn (Mar spike driven by LFT rollover); H2/26 = R$807.8bn (Aug spike driven by NTN-B). Source: DPMFi Feb/26 report.

| Instrument | Heaviest Maturity Months | Common Maturities Issued | Treasury Rollover Strategy |

|---|---|---|---|

| LFT Floating / Selic |

Mar 2027 (~R$490bn) Sep 2027 |

Mar 2032 (primary benchmark) | Aggressively rolling legacy 3-yr debt into a single 6-yr benchmark to reduce single-month cliff risk |

| LTN Zero-coupon fixed |

Jul 2026 (R$251.7bn) Apr 2027 |

Apr 2027 (12m) Jan 2032 (72m) |

Establishing 6 tenors (6m–72m) to distribute redemptions and avoid single-month spikes |

| NTN-F Fixed 10% semi-annual coupon |

Jan 2027 (~R$310bn+ principal + coupons) | Jan 2031 (5-yr) Jan 2037 (10-yr) |

Shifting the "January wall" from 2027 into 2031/2037 benchmarks to extend duration |

| NTN-B IPCA + real yield |

Aug 2026 (R$288.4bn) May 2027 |

May 2031 Aug 2040 (standard tenors) |

Offering IPCA + 6% to prevent EFPCs (pension funds) from selling into the secondary market |

Source: DPMFi Feb/26 report. H1 avg R$163bn/month, H2 avg R$140bn/month — Jan/25 through Dec/25.

Source: STN/Tesouro Nacional RMD Fev/26 (Anexo 1.6). Dívida Mobiliária (global bonds) only; R$ billions. 2015 and 2022 = zero issuance. Note: BRL depreciation inflates later years in BRL terms.

The Treasury maintains a cash buffer equivalent to 6–9 months of upcoming maturities, held in the Conta Única at the BCB. This reserve is used opportunistically — the Treasury can step back from primary auctions when market conditions are unfavorable (high risk premia, stressed liquidity) and draw down the buffer instead. In practice this means issuance over-shoots financing needs in benign conditions and under-shoots during stress. The buffer also provides fiscal credibility: it insulates near-term debt servicing from short-term market disruptions.